Let’s work together to find a solution

Rely on AVANA Capital to help preserve your wealth and create growth for your business.

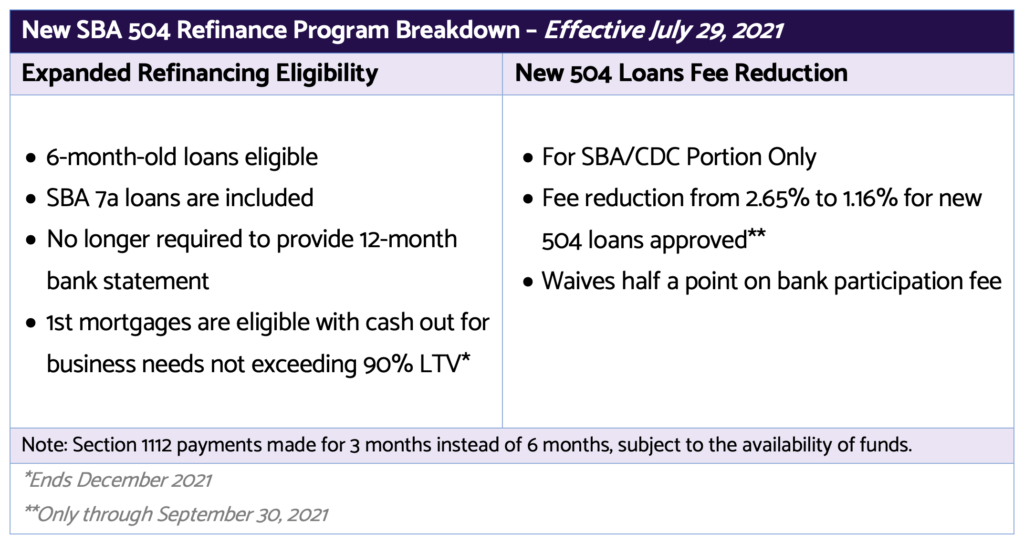

Effective July 29, 2021 business owners can now save money and refinance existing conventional loans, SBA 7a loans and SBA 504 debentures. A new rule was just enacted by the US Small Business Administration (SBA) to better meet the debt refinancing needs of small businesses.

The SBA expanded the 504 Loan Program and made permanent changes to allow small business owners to refinance existing debt and tap the equity in their owner-occupied real estate to obtain cash to grow and expand their business. An SBA 504 loan is a loan guaranteed by the federal government. This program combines a conventional loan from a private lender in a first lien position with a 100% government guaranteed loan in a second lien position from the SBA.

Since the start of the pandemic, a variety of support has been offered by the US government — from grants to tax relief to loan repayment deferrals — to assist small businesses during these challenging times.

The 504 Loan Program is one of these financial support mechanisms. 504 loans can provide capital to businesses when conventional lenders are becoming more cautious due to economic uncertainty and are a tool that benefits both borrowers and lenders with low borrower interest rates coupled with low lender advance rates. With the new rule, the SBA aims to provide greater flexibility and benefits to small businesses in restructuring their debt and economic relief to small businesses negatively impacted by COVID-19.

Additional details on the change include the following:

This interim final rule implements section 328 of the Economic Aid to Hard-Hit Small Businesses, Nonprofits, and Venues Act, which adjusted the debt refinancing requirements of the 504 Loan Program. The revision increases the allowed debt limit that may be refinanced for debt refinancing involving expansions. It also removes two limitations for 504 debt refinancing not involving expansions by first reinstating an alternate job retention goal for the refinancing project, revising the definition of qualified debt, and lifting the ban on Certified Development Companies (CDCs) that participate in the Premier Certified Lenders Program.

For more information on AVANA Capital’s long-time experience with SBA 504 Loans as well as more information on the loan requirements, please see our Preserver article from earlier this year and visit the SBA website.